Published March 28, 2017 by SmolenPlevy

Tax issues can surface every year, but former spouses who continue to feud lose the opportunity to save themselves taxes. The Wall Street Journal shares six tax issues that could affect you if you are divorced.

Divorce has many miseries. Taxes are one of the most persistent.

Issues can resurface annually during filing season and continue to affect couples years after they split. If former spouses don’t set aside their differences, one or both partners often end up overpaying.

Scott Kaplowitch, a managing partner with Edelstein & Co. in Boston, recently prepared a divorced couple’s returns. Although the ex-wife had the right to take deductions and credits for the couple’s children, there was no benefit for her because she has no employment income. She allowed her former husband to use the tax breaks and saved him about $2,500, Mr. Kaplowitch says.

The couple didn’t split the savings, he adds, but “it produced good will for the future.”

That’s the best case.

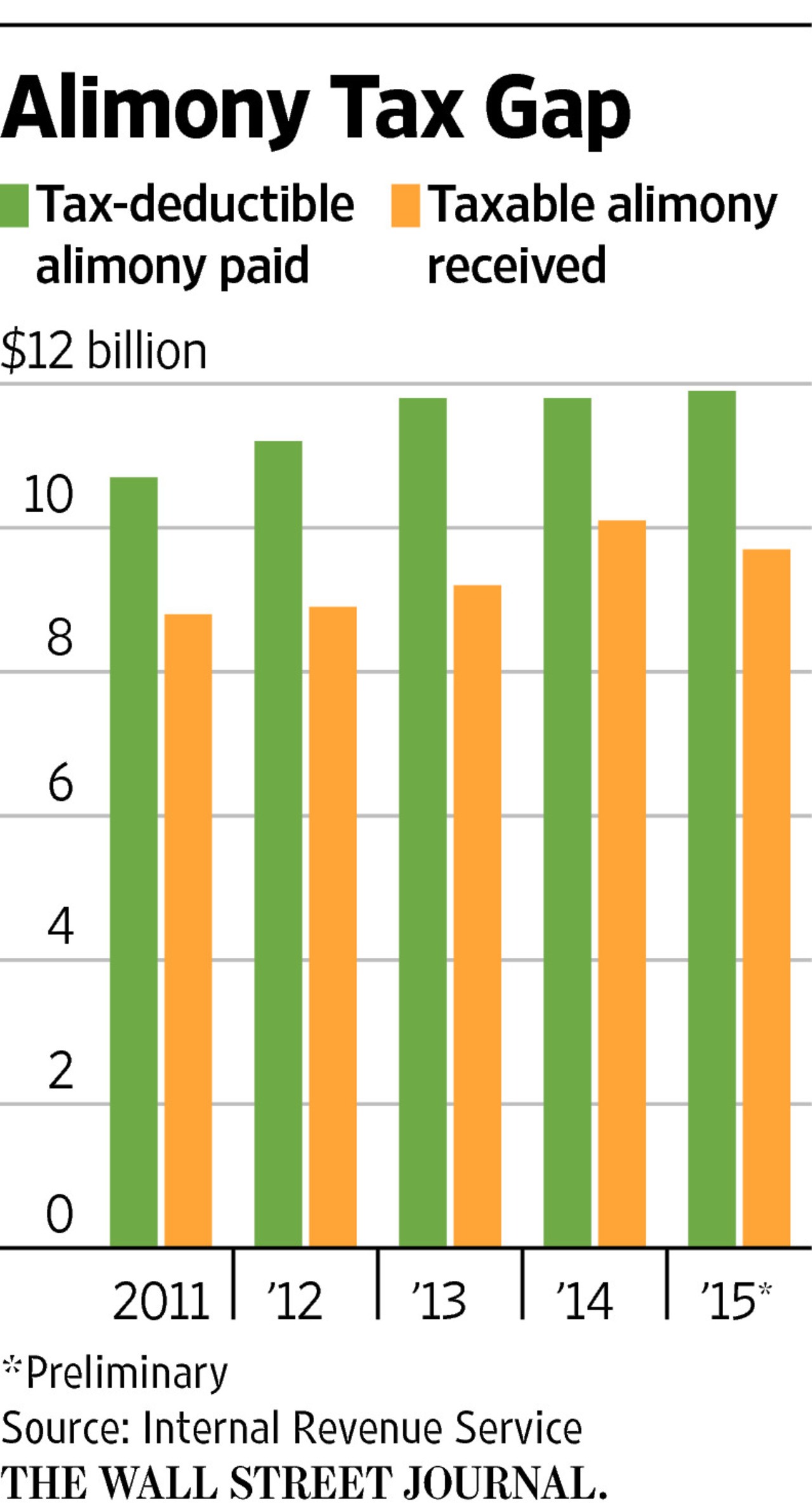

Tensions between ex-spouses are evident in Internal Revenue Service data. For the five years that ended in 2015, people paying alimony deducted some $57 billion, while people receiving alimony claimed only about $47 billion—a $10 billion discrepancy.

After a Treasury watchdog chided the IRS about the alimony gap in 2014, the agency became more vigilant. Now returns are automatically rejected if the alimony payer doesn’t supply a Social Security number for the recipient, an IRS spokesman says.

If you’re divorced, here are tax issues to watch.

Alimony. These payments, often called “maintenance,” are deductible by the payer and taxable to the recipient. To be deductible, payments must be made in cash and must be provided for in the divorce or separation agreement.

Voluntary payments for other items, such as a new computer for a child, typically can’t be deducted. The IRS has a history of challenging alimony deductions it thinks are nondeductible property settlements, child support or gifts.

Alimony can fund an individual retirement account. Alimony deductions end when the recipient dies, if payments haven’t already ended. For more on the definition of alimony, see IRS Publication 504.

Child support. These payments aren’t deductible by the payer or taxable to the recipient.

Dependent exemption. This benefit is a deduction, currently $4,050 for each child who qualifies as a dependent. There are several tests for this benefit, and they are detailed in IRS Publication 501.

Ex-spouses can often use IRS Form 8332 to toggle this exemption back and forth from year to year. This can be a good strategy if one ex is sometimes a high earner, because in 2016 the exemption began to phase out at $259,400 of adjusted gross income for single filers.

For feuding ex-spouses, there is an important caveat: The parent claiming the dependent exemption must include each child’s Social Security number, and the IRS’s system will reject a later-filed return claiming the same number. Even if the second-filing spouse deserves to take the exemption, the IRS seldom has the resources to sort out this issue, experts say.

Tax credits. These valuable breaks offset taxes instead of merely reducing income, and in some cases they can result in a refund check for a taxpayer who owes no tax. Tax credits involving children typically go to the spouse claiming the personal exemptions for them.

The Child Tax Credit of up to $1,000 per child began to phase out at $75,000 for single filers in 2016. The Earned Income Credit, which benefits the working poor, was up to $6,269 for single filers with three or more children and income up to about $48,000. The Dependent Care Credit, which is up to $2,100 for two or more children and $6,000 of total eligible expenses, has no income limit.

Education benefits. For most people, the best tax break for college is the American Opportunity Credit, which can reduce taxes by as much as $2,500 on up to $4,000 of college expenses per child.

Single filers get a lesser break or none if their income exceeds $80,000, but in some cases the child can benefit by claiming the credit if neither parent can—even if the child doesn’t pay the tuition.

Taxes on a residence. To take typical homeowner deductions for mortgage interest or property taxes, a person must have full or partial ownership of the home and actually pay the expenses.

What if a home is sold and the proceeds divided? Each ex-spouse can get an exemption of up to $250,000 of gain, as long as that person both owned the home for two years and used it as a main residence for two years. For more details, see IRS Publication 523.